Relevant for students of AAT Level 2 Elements of Costing. Four tasks on a spreadsheet, presenting assorted data that needs to be rewritten in the sequence of a Manufacturing account. Last two tasks also require subtotals to be calculated. Answers provided, on page 2 so can be printed with or without.

Relevant for AAT Level 3 students of Accounts Preparation unit. This is a traditional cut-out-and arrange game. Account names and balances on one sheet are to be cut out and jumbled up. Instructions sheet provided. Task 1 is to arrange the cut-outs into an initial trial balance (2 columns). Task 2 is to arrange the cut-outs into an extended trial balance (4 columns). Answers provided.

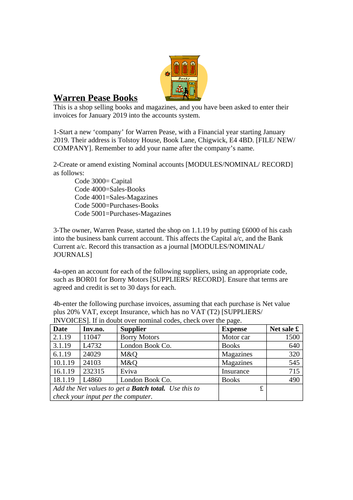

Relevant to students of AAT Level 2 Using Accounting Software. This activity requires users to set up a new company, amend General Ledger account names, and input by Journal the owners Capital Introduction.

The main tasks then are to create 4 Supplier records and input 6 purchase invoices, followed by 5 Customer records, and 6 sales invoices. Users can then self check a Trial Balance.

Useful as a reinforcement or extension activity.

Relevant for students of AAT Level 2 Using accounting software.

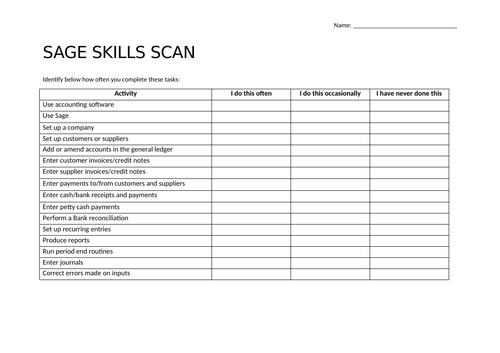

Simple self assessment for users of their previous experience in using Sage software. Contains sixteen questions. To be used and analysed at start of the unit.

Relevant to AAT Level 2 Elements of Costing. This activity requires students to complete a stock record card-calculating an issue price, and the balance of inventory value. Three sections-FIFO, LIFO, AVCO. Additional task requires students to calculate Sales, Cost of Sales and Gross Profit under the three methods. Illustrates which method may give highest inventory value, highest profit, etc.

Students can complete on paper or in Excel. Answer is provided.

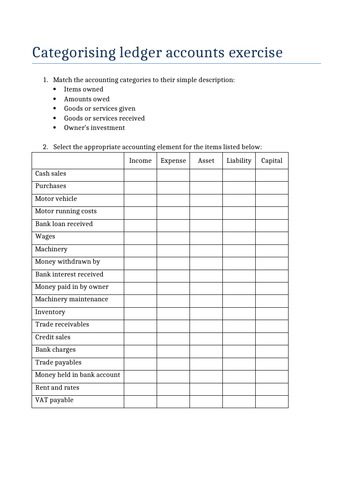

Relevant to AAT Level 2 Bookkeeping Transactions unit. Task 1 asks students to match the definitions with the correct accounting category (Income, Expense, Asset, Liability, Capital), while task 2 presents 19 ledger accounts to be similarly categorised. Task appropriate for early stages of bookkeeping course.

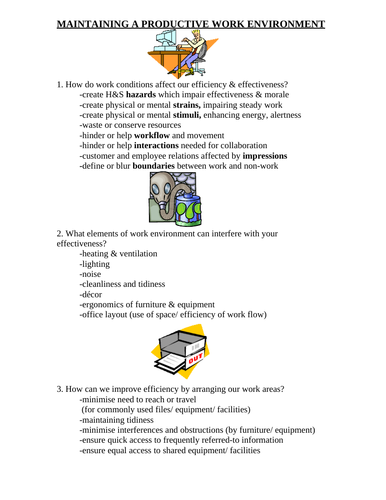

Relevant to AAT Level 2 students of Working Effectively in Finance unit. Two pages of notes, and clipart, to encourage discussion on work conditions, and interferences, ideas for improvement, showing a professional image, and maintaining work equipment.

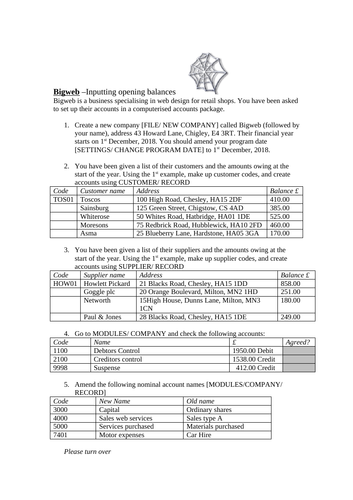

Relevant for students of AAT Level 2 Using accounting software. This activity requires the user to set up a new company, enter and code 5 customer records, and 4 supplier records, each with opening balances. Further activity requires account names to be amended, and general ledger opening balances to be entered. The last task requires the Trial balance to be self checked by the user.

Useful as reinforcement or as an extension activity.

Relevant for AAT Level 2 **Using accounting software **unit. Good as demonstration, short reinforcement, or extension activity (textbooks often only offer this activity as part of a larger and long project). The exercise requires students to set up a company, enter bank payments and receipts, calculate the initial difference between bank statement and Sage, reconcile transactions and produce a report. It is appropriate for use after initial guidance on these steps. Can be self checked by students as the calculation should agree with the report.

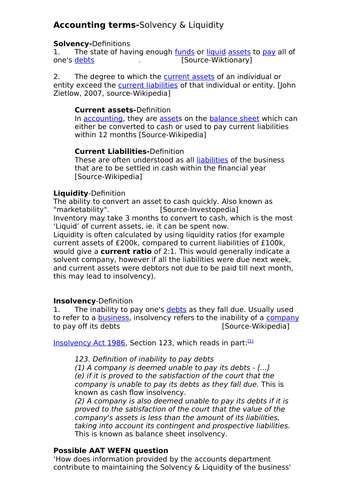

A four page document with

-definitions of Solvency, Insolvency and Liquidity

-possible AAT WEFN question, with suggested answer

-three exercises categorising assets and liabilities and assessing Solvency, Liquidity and Current Ratio.

Aimed at Level 2 students, but also relevant to Level 3.

Separate Answers sheet

This worksheet is relevant to many accounting exams for Basic Costing (sometimes under the Management Accounting heading).

It should be used after explaining what Fixed, Variable, and Semi-Variable costs are in principle.

Common exam questions present a scenario where the Total costs are known at two or more production levels. The task may then require the student to calculate costs at other production levels, which first entails calculating Variable costs per unit, and Total Fixed Costs.

The worksheet gives a worked example with a step by step guide to the HILO method of calculation.

This is then followed by three exercises for the student to try, and a separate Answer sheet. While the first two exercises only require the Total Variable Costs and Total Fixed Cost to be calculated, the 3rd exercise also requires the Total cost at a new level to be calculated.

This is a traditional gap exercise, whereby one figure is given and students need to calculate the missing figures.

Suggested formulae are given using percentages (you may wish to also give formulae based on fractions).

A short extension exercise encourages students to work out the formulae if the VAT rate became 25% (VAT rate has remained 20% for many years, but can change).

A separate answer sheet is also given which you could use as your own crib sheet, or hand out to students later.

You may wish to point to the numeric patterns within the formulae, and encourage them to work out formulae if the VAT rate became 17.5% (which it once was-here fractions were easier-e.g. gross £1175 x 7/47 gives £175 VAT) or 15% or 10%.